It has been a quarter of increased volatility in equity markets, but one must remember that this is coming from the starting point of markets at all-time highs and buoyant investor sentiment.

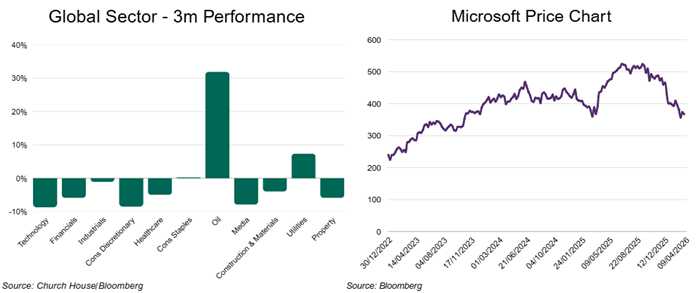

One look at the chart, right, detailing global sector performance says it all – Q1 2026 was all about oil stocks.

All the oil majors posted strong share price gains over the period, with Exxon Mobil leading the pack at +41%, BP just behind at +40% and the likes of Chevron and Shell also making handsome gains. The price of oil has potentially peaked but either way, these companies will be receiving in the region of twice the price for their barrels of oil in 2026 than they did last year and this goes straight to the bottom line.

Defence companies have also been beneficiaries of escalating hostilities in the Middle East. From RTX Corp, who supply everything from Pratt & Whitney jets to Raytheon missile, radar and communication systems, to Britain’s BAE Systems, who specialise in naval ships and fighter jets, demand is (sadly) high and unlikely to abate any time soon.

Semiconductor stocks and the wider technology sector were the primary driver of market returns in 2025 and this has become a more nuanced picture of late. Shares in semiconductor bellwethers Nvidia and Broadcom have paused for breath, unable to break to new highs despite excellent recent results, but the biggest moves have been in the software space. While investors spent 2025 enthusing about the growth opportunities around AI, 2026 has seen the mood sour, instead focusing on perceived AI losers. There were a feverish few weeks in the quarter where the investors were climbing over each other to exit their software stocks, sending the whole sector down, even the likes of Microsoft were not immune, with shares down 23% in 3 months. The market has since begun to pick through the bones of this indiscriminate sell-off, albeit these names remain soundly beaten-up.

Whisper it gently, the UK has been the top performing major global market in 2026. The FTSE 100 has benefitted from its relatively larger weightings to oil and defence companies, up 2.0% year-to-date, compared to the S&P 500 -4.6% and Euro Stoxx 50 -3.8%. After years spent out in the cold, let us hope the London markets can regain some of their previous status.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note that the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?