Inflation fears, geopolitical tension and the uneasy calm beneath record stock prices

Market Snapshot - Relief Rally Takes Hold

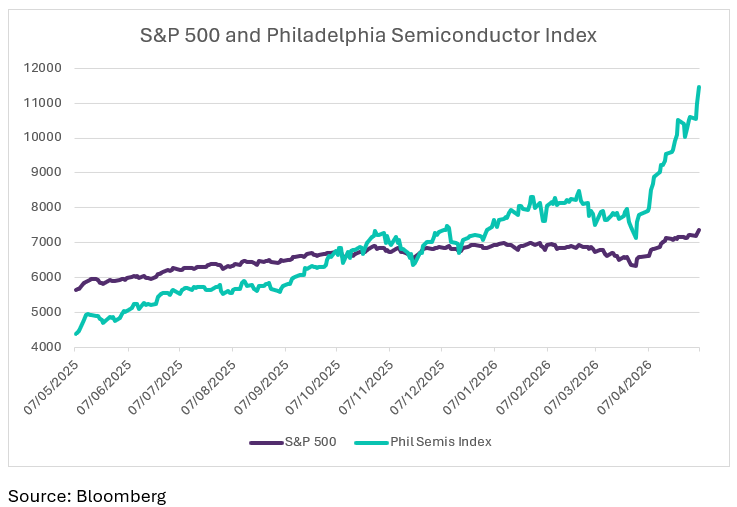

Equity markets only needed a whiff that a US-Iranian ceasefire was in the air for the bulls to be let loose. Since bottoming on 30th March, the S&P 500 Index has been on a tear, rising by 16.1% to 6th May, breaking back above all-time highs.

AI Still Trumps Everything Else

As has been the case for several years now, US Tech led the way, with the Nasdaq Index popping 24.6% over the same period. But that is nothing in comparison to the Philadelphia Semiconductor Index (made up of companies involved in the design, manufacture, and sale of semiconductors) - up a cool 60.6% in just over a month of trading. US equity markets have definitively voted that events in the Gulf are inconvenient but pale in comparison to the might of AI-driven growth closer to home. Bond markets are telling a different story.

Bond Markets Disagree - Inflation Risks Persist

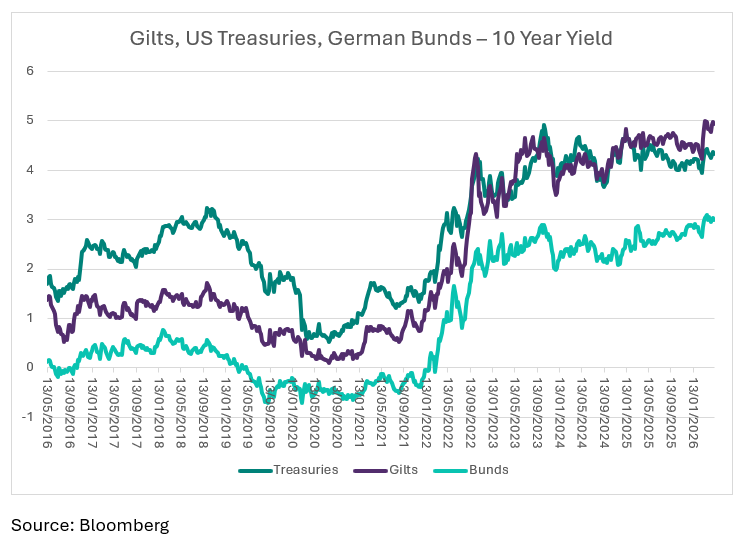

Through March government bond yields rose across the developed world, reflecting heightened geo-political tension and, particularly, expectations of higher inflation; and these remained resolutely higher in April. 10-year gilt yields have been testing the 5.0% level for a few weeks now – comfortably above borrowing costs hit during both the Liz Truss premiership and the Russian invasion of Ukraine.

Why the Bond Market May Be Right

The adage about bond markets being more reliable indicators than equities is hard to ignore. Bond markets share our view that a clean “deal” and return to normal service in global commodity markets is pie in the sky. The idea of the Iranian régime giving up their ace card (the Straits of Hormuz) in the near-term without material concessions is not what scientists would call a working hypothesis (i.e. not likely) and so we must expect commodity markets to remain elevated, leading to higher prices for all. We saw from the latest round of central bank comments that the bankers are all sitting on their hands for now, hoping that the situation will resolve itself and this bout of inflation can be discarded as transitory. But this is not a given.

Geopolitics in Practice - Diplomacy, Ego and Compromise

We recently hosted the fascinating Lt. Gen. John Cooper (former Deputy Commander of Multinational Force-Iraq, among many other appointments) for a discussion and he made the point that diplomacy is at its heart all about people, relationships and ego. Seemingly without the willingness to commit the boots to ground that are required to drive régime change in Iran, US authorities are forced to work with the existing régime and offer them more than the threat of more missiles to make progress.

Conclusion - Hope, Not Yet Resolution

The release of the billions of Iranian state and private assets currently frozen appears a good starting point and one that could be massaged suitably to allow Donald Trump to keep face. This would effectively be paying the Iranian leaders to reopen the Straits (because that cash isn’t going to the suffering Iranian people) and both sides could claim victory in their own media, while equity markets firmly turn back to AI-excitement and bond yields moderate.

Here’s hoping.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note that the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?