2024 certainly had its moments, now we head into the first year of a second term for Donald Trump, and this time he appears to have control of the legislature as well.

The central banks didn’t altogether play ball in 2024, the US Federal Reserve and the Bank of England have held rates higher for longer than expected. But it is hard to carp at the Federal Reserve, which does appear to have played its hand to perfection and is delivering on the hoped for ‘soft landing’.

The Bank of England is in a bit of a bind with the economy apparently moribund, while service inflation (and wage growth) remains high enough to deter them from cutting rates any faster. But these are worries that lag and companies are less likely to be in the mood for further wage rises after the National Insurance increase. The Bank of England is likely to resume its cuts over the first quarter. The Federal Reserve ‘disappointed’ with a quarter point cut to 4.5% in their base rate in December but a decidedly more ‘wait and see’ tone to Chairman Powell’s comments. With a capricious new President about to move into the White House this looks sensible.

Interest rates for longer periods have been on the increase as markets return to worrying about where the money is going to come from to fund budget deficits. The UK ten-year Gilt yield, that started the year at an exuberant 3.6%, has been going up for the past three months now to close at 4.6%; further out it has been even more miserable for bond investors with the thirty-year Gilt yield back over 5% again. US bond yields have followed a similar pattern with the ten-year US Treasury yield close to the high for the year at 4.6% (in-line with the UK Gilt).

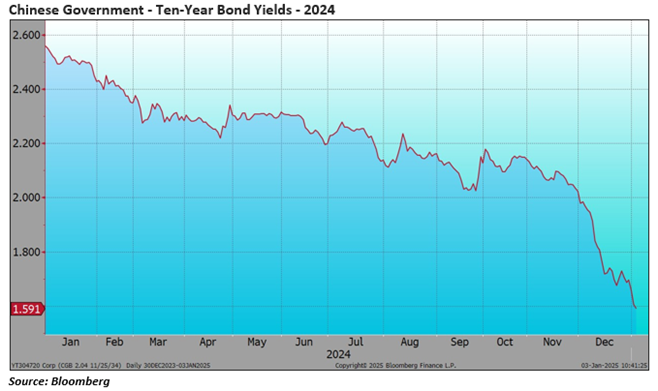

For a stark contrast, take a look at the course of Chinese ten-year government bond yields, right , methinks they are more concerned with deflation than inflation… (why would anyone want to buy these bonds when they can get 4.5% on a US Treasury?)

After the exuberance of November, US stocks turned a lot more volatile in December and the S&P 500 actually fell over the month. The commentary from the Fed along with more analysis (!?) of President Trump’s apparently contradictory policies and the potential impact of trade sanctions, introduced a necessary element of doubt. London stocks followed suit with a dull month of modestly negative returns while German and French stocks rose. German stocks have been the surprise star turn for the year with a gain of 19% for the Dax Index despite ongoing political concerns.

There would appear to be a lot of enthusiasm priced-in to US equities, so it would not be a surprise to see them disappoint over 2025, on the other hand US Treasuries are looking attractive by comparison. In the UK, equities remain cheap (with a ‘UK for sale’ sign prominent) but Gilts also look to be at the attractive end of the range.

And now for some wishful thinking… The ‘Red Sweep’ of deregulation that is supposed to be about to hit US Government departments could work, whatever one might think of Elon Musk (and his new DOGE) he is certainly prone to radical ideas. It doesn’t feel like there is a Regan era understanding of the problem yet, but maybe that is too pessimistic, it could be transformational (not to mention v bullish for US Treasuries). In the Middle East, the extraordinary events in Syria have completely changed the dynamic leaving Russia and Iran looking foolish (and friendless). Inflation is taking off again in Russia thanks to their extraordinary expenditure on defence (and ghastly expenditure of lives) and the ruble is heading down again (see right). Inflation certainly did for the US democrats (and was a final nail for the Tories here), as a last leap in wishful thinking perhaps it could for Putin too…

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?