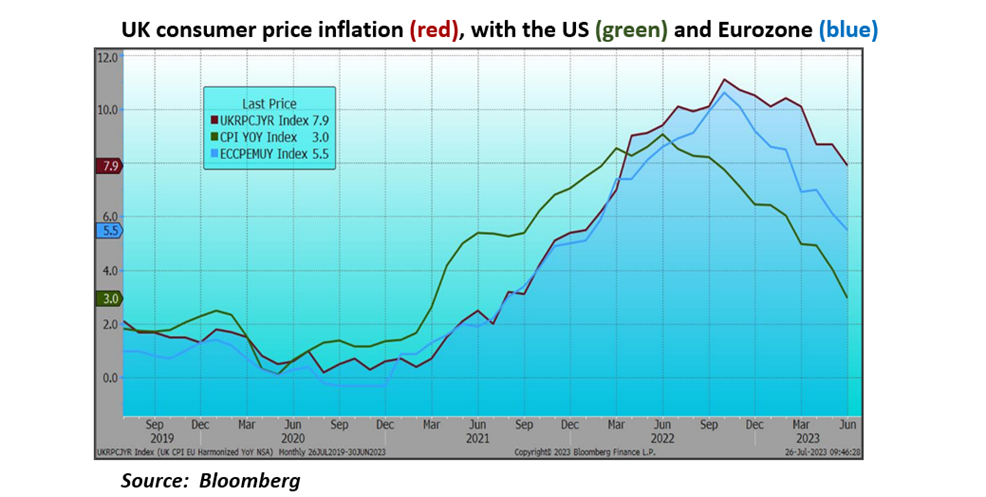

That ‘sticky’ inflation: July has brought some slightly improving news for the UK as consumer prices edged down again in pursuit of US and European rates, right.

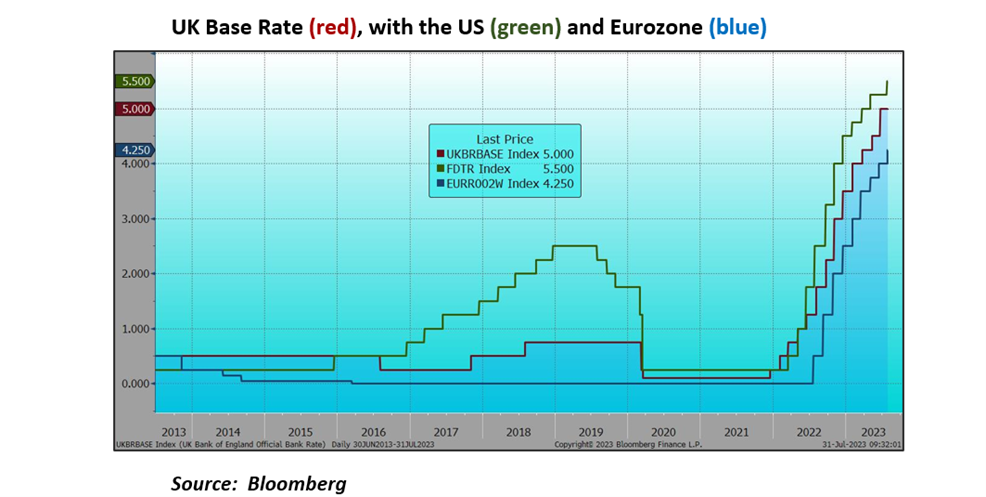

The US Federal Reserve ended its pause on rate increases with a further ¼% rise to 5.5% as expected and the European Central Bank (ECB) raised theirs to 4.25% the following day, again as expected. Both left the door open for further increases in the autumn while being ‘data dependent’, a still robust US economy looks the more likely candidate. Now we wait for the Bank of England this week with most expecting a ¼% increase but some pushing for another ½% move. The air of uncertainty around the Bank’s actions being rather (unfortunately) symptomatic at the moment, right.

The ECB has probably completed its hiking cycle now while the Federal Reserve and the Bank of England are almost there. The novelty that has been thrown into the mix this week is the Bank of Japan’s decision to bring ‘flexibility’ to its long-standing YCC (yield curve control) policy and Japanese rates are finally being allowed to rise (a bit!), it appears likely that the YCC will finally be removed before the end of the year. China is moving in the opposite direction, easing rates in an attempt to bolster their stalling recovery.

We still don’t know how much damage has been inflicted on economies by that steep rise in rates and probably won’t for a while yet. In the US, the economy usually heads into recession around a year after their yield curve first turns negative (short rates moving higher than long rates), which would indicate some time around October. But, for now, Goldilocks reins supreme, inflation is falling, and their economy remains remarkably resilient. Maybe the tighter monetary policy has merely counter-balanced the massive fiscal boost they got from the Biden administration… Maybe it’s different this time…

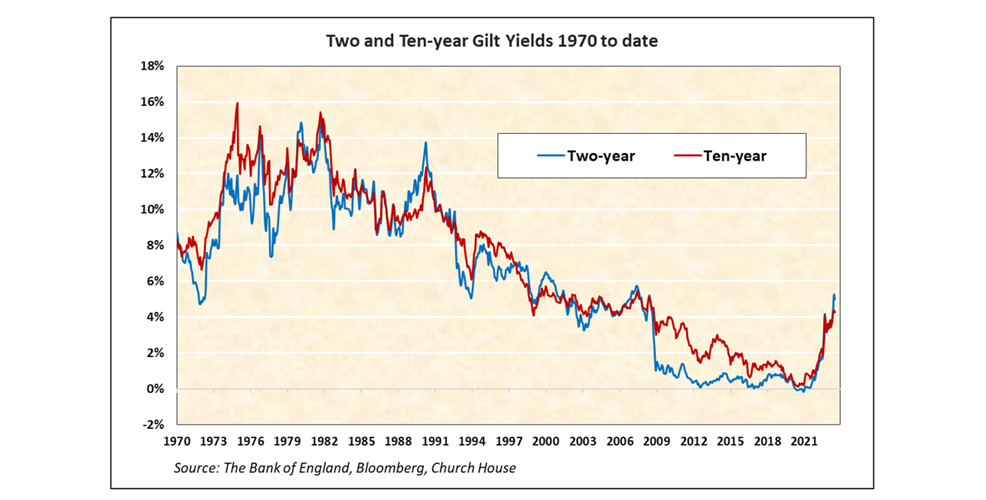

The link between an inverted yield curve and recessions is not as clearcut in the UK but it does normally herald a general fall in rates. Our longer-term chart of two-year Gilt yields v. ten-year Gilt yields illustrates the point (the yield curve is ‘inverted’ whenever the blue line moves above the red line, right).

Back to the here and now and the improvement in UK inflation brought some relief to Gilts. But, after a torrid start to the month, longer-dated bonds are still down around 2.5% over the month (yield up to 4.5%) while the ten-year is unchanged (yield at 4.35%). In the US and Europe Treasury and bond prices weakened across the board.

Equity markets, principally the US equity markets, are in thrall to Goldilocks (shortly to be replace by Barbie) and stocks have had a good month. The NASDAQ has led again (up more than 5% over this period) in turn led by yet more good figures from big tech. Alphabet and Meta Platforms led the way with gains of 10% or more, Microsoft paused after their phenomenal first half. Lesser names (these days) like IBM and Intel were close behind after their figures. This week brings figures from Apple and Amazon, I hope they don’t disappoint. The financial sectors also put in a good showing after the round of reports from the banks, Bank of America, Mitsubishi UFJ Financial (all the Japanese banks shone as the YCC moved towards its end), JP Morgan, Banco Santander and Standard Chartered were all good features.

It was a dull month for the oil majors with Exxon Mobil and Shell reporting steep falls in profits and their stock prices were little changed. But the price of oil has picked up after the falls over the year to date and this could easily return to take some of the shine of the falling inflation party.

We note that many commentators have picked-up on our ‘generational shift’ in rates remarks last month. We still think that the UK short-dated fixed interest market is attractive now and corporate credit particularly so. We do think that it is important to stick with quality and investment grade issues, further down into high yield and junk there is likely to be a lot of pain as re-financing comes around.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?